Sunday Essay · Oil Sector Policy

A decade after its signing, Guyana’s 2016 Production Sharing Agreement is less a commercial instrument than a confession — about how small we still understood ourselves to be, and about the political habit that keeps that smallness in force.

Brooklyn, New York · April 26, 2026 · By Dr. Terrence Richard Blackman

Every postcolonial state inherits a ledger it did not open and cannot yet close. The entries were made before independence, in languages the new state would not speak, by hands that would not stay. Independence did not erase the ledger. It only transferred the obligation to balance it.

On June 27, 2016, amidst a period of political transition and thinned institutional capacity, the Government of Guyana signed a Production Sharing Agreement with ExxonMobil, Hess Corporation, and CNOOC Nexen Petroleum Guyana Limited for the 26,800-square-kilometer Stabroek Block. The document superseded a 1999 accord signed under the Janet Jagan administration and sat atop seven other deepwater contracts executed between 1999 and 2015 on substantially the same template. In the official language of the day, the 2016 PSA was described as a necessary act of de-risking: the Liza-1 discovery of May 2015 had not yet ripened into the eleven-billion-barrel province we now know it to be, the Venezuelan claim on Essequibo was freshly active, and the Guyanese state, by any honest measure, lacked the technical and legal capacity to sit across the table from counsel that had drafted concessions on four continents. A decade later, those framings have acquired a different weight. What Guyana signed that day was a commercial instrument. It was also — and this is the harder thing to say — a confession about how small we still understood ourselves to be.

This essay is about that confession, about what it costs us now, and about why neither of the parties that have governed Guyana since Independence has been able to rescind it. It is not, in the first instance, an essay about royalty rates or cost recovery ceilings or ring-fencing provisions, though we will come to all of these. It is an essay about consent — about who has the standing to give it, what it obligates us to, and what moral inheritance accumulates when a generation of leaders decides that the terms of the nation’s diminishment are, on balance, the terms it can live with.

Three questions will guide the analysis. Who consented, on whose behalf, and to what? What architecture of reasoning keeps that consent in force against every subsequent revelation about its inadequacy? And what does sovereignty require of us now, as the block delivers over nine hundred thousand barrels a day and the Natural Resource Fund passes three billion dollars on its way to a number no one in 1999 could have written down without flinching?

2%

Royalty Rate

in 2016 Stabroek

PSA

75%

Monthly Cost

Recovery Maximum

2016 Stabroek PSA

$8.7B+

Cumulative Oil

Revenue to NRF

(2020-2025)

11B+ BOE

Estimated Recoverable

Resources in

Stabroek Block

Section I

The Inheritance: 1999, the Seven Silent Years, and the Moment We Missed

Guyana’s oil history is older than the 2016 agreement and older than the 1999 one. It begins with decades of exploratory disappointment — dry holes offshore Essequibo from the 1940s forward, a basin the majors wrote off as technically interesting and commercially hopeless. It is that long arc of discouragement that produced the generous frontier terms of the 1999 PSA between the Janet Jagan administration and Esso Exploration and Production Guyana Limited. A one percent royalty. A fifty-fifty profit-oil share after cost recovery. No ring-fencing. No signature bonus of consequence. In 1999, these terms were not, in any formal sense, generous; they were what frontier basins of unproven commercial viability commanded from sophisticated operators at the end of a century in which more than forty wells had been drilled offshore Guyana and none had produced a barrel.

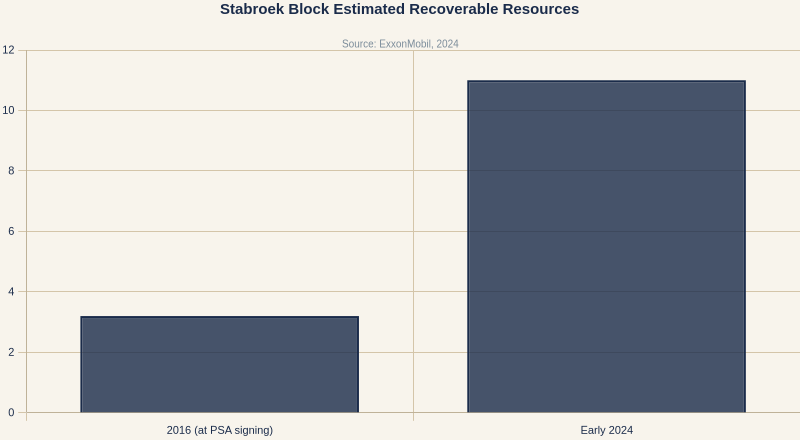

What happened next is harder to defend. Between 1999 and 2015, successive administrations signed approximately seven additional deepwater contracts using the 1999 template virtually unchanged. The template ossified into doctrine. When, in May 2015, the Liza-1 well hit commercial pay at 5,719 feet of water, the geological story of the Guyana basin was rewritten overnight. Within months, the basin was understood to hold not one commercial discovery but a cluster; within two years, proven recoverable resources had grown to over three billion barrels of oil equivalent; within a decade, to more than eleven billion. The contract, however, did not change until June 2016 — and when it did change, it changed at the margins.

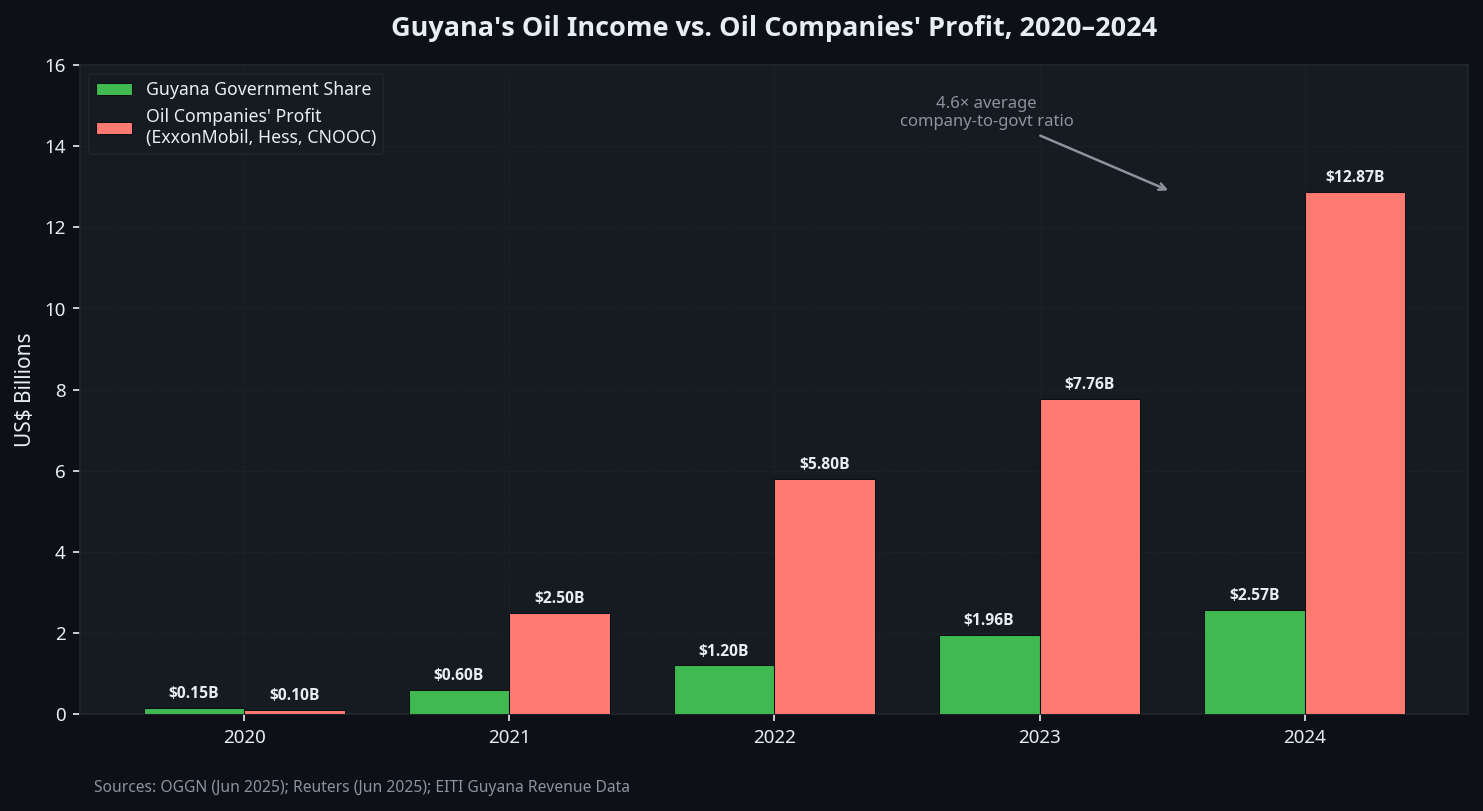

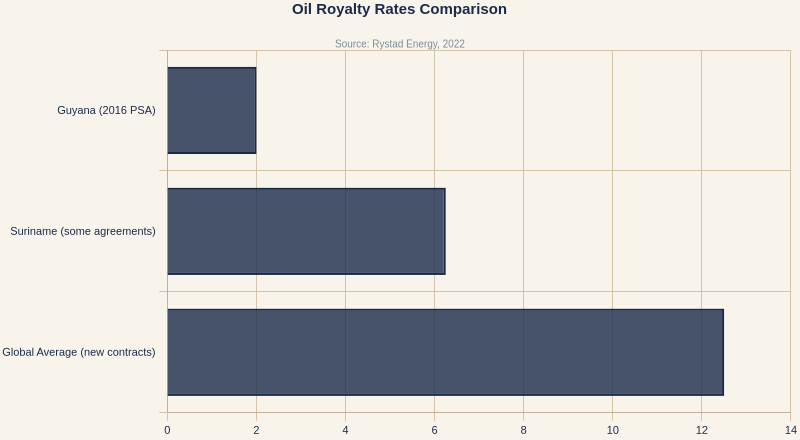

The APNU+AFC government that signed the 2016 renegotiation did so with Liza already drilled and commercial. The operator knew what it had. The state could reasonably have priced the certainty. Instead, the renegotiation preserved the frame of the 1999 agreement and adjusted its fiscal terms at the hem. The royalty rose from one percent to two — an increase the government of the day celebrated as a doubling, though the arithmetic reveals it as the smallest double any finance minister will ever announce. The cost-recovery framework was retained. Ring-fencing was not introduced. An eighteen-million-dollar signature bonus was accepted. No competitive bidding round was held. As Dr. Vincent Adams has observed, the 2015 discovery had added approximately two hundred billion U.S. dollars to ExxonMobil’s book value — a valuation shock that rearranged the bargaining power between the contracting parties in ways no responsible state could have ignored. Given the proven resource and the queue of competitors who would have taken ExxonMobil’s place on a phone call’s notice, Adams argued at the time, Guyana should have demanded an up-front payment of no less than one billion dollars (Stabroek News, 2018). We did not. We accepted eighteen million. This is not a failure of arithmetic. It is a failure of posture.

The International Monetary Fund, in each of its subsequent Article IV consultations, has reached the same conclusion through more diplomatic prose: that the institutional architecture through which Guyana negotiated in 2016 — the Ministry of Natural Resources, the Guyana Geology and Mines Commission, the Attorney General’s Chambers — was not sized to the task placed before it (IMF, 2017; 2021; 2023). This is true. It is also beside the deeper point. Institutional capacity can be built; it cannot be retrofitted onto a contract already signed. What the 2016 negotiation reveals is not only a technical deficit. It is a habit of mind.

GBJ Data Note

The 2016 Stabroek Block PSA stipulates a 2% royalty on gross production and a 75% monthly cost-recovery maximum. The royalty is significantly below the global average for new oil contracts, which typically ranges from 10% to 15%, and below several Caribbean-region contemporaries — including Suriname’s 6.25% royalty rate on some of its more recent deepwater blocks (Rystad Energy, 2022). The disparity is not a rounding error. It is the measure of what was left on the table.

Section II

The Architecture of Resignation

The habit of mind has a name, and it was named almost half a century ago.

Lloyd Best and Kari Polanyi Levitt, in the plantation economy literature of the early 1970s, taught us that Caribbean economies are not merely small and open; they are structurally configured to transmit metropolitan decisions with minimal resistance. The plantation, as an institution, was designed to be negotiated on behalf of. Its operators lived elsewhere, drew profits elsewhere, made capital decisions elsewhere. The local elite’s function, whether under slavery or after, was not to bargain but to administer — to keep the throughput steady and the terms accepted. When independence arrived, Best argued, the ownership plaque changed but the administrative posture did not. The plantation’s grammar of consent — consent that is given because refusal is believed to be impossible — remained the grammar of postcolonial statecraft.

This is the deeper sense in which the 2016 PSA is a plantation document. Not because its terms are exploitative, though several are. Not because ExxonMobil is the reincarnation of Bookers McConnell, though the rhyme is available. But because the form of consent it elicits from the Guyanese state is the plantation form: the state accepts terms it did not set, under conditions it cannot independently verify, for reasons it cannot fully audit, because refusal is understood to sit outside the grammar of what a small economy can do.

Albert Hirschman, writing from a different tradition, offered the three options available to members of a declining organization: exit, voice, loyalty. The plantation economy preemptively collapses two of them. Exit is not available to the sovereign; the basin is where the basin is, and the state cannot move itself somewhere it is more respected. Voice is available in principle but requires institutional infrastructure — courts that can enforce, ministries that can audit, publics that can mobilize — that the plantation state has historically been configured not to develop. What remains is loyalty. Loyalty, in this context, does not mean affection. It means the acceptance of the terms of membership as they are, because the cost of contesting them is understood to exceed whatever contestation could win. It is not, in other words, that the PPP/C loves the 2016 contract or that APNU+AFC loved it when they signed it. It is that both governments have made the same calculation about what voice would cost — and have critiqued the other, in opposition, for making precisely that calculation in government.

Thomas Schelling, whose work I have drawn on before in these pages, would recognize what is happening here as a focal point equilibrium. The “sanctity of contracts” is not, in the Guyanese case, a settled principle of international commercial law; international commercial law is in fact quite accommodating of renegotiation under changed circumstances. It is a coordinating convention — a story that domestic elites and international counterparties tell each other so that they may know, in advance, how the other will behave. Once the convention is in place, violating it carries costs that exceed the bare legal exposure: it becomes a signal about what kind of state Guyana is, read by investors, rating agencies, and bilateral partners who have not actually read the contract but have read the signal. Sanctity, in this sense, is not a law. It is a reputation technology. The question this essay is actually asking is whether the reputation it buys is worth what it costs.

Resignation, named this way, is not a single thing. It is the convergence of three distinct forces, and separating them is the analytical work the rest of this essay will do. The first is legal constraint — the stability clauses and consent requirements written into the 2016 document itself, which are real but narrower in their reach than either proponents or opponents of renegotiation routinely claim. The second is political risk — the investor signal, the arbitration exposure, the rating-agency reaction — which is also real and also routinely overestimated, particularly in a basin where the queue of willing operators is long. The third, and the most decisive, is imaginative failure — the inability of a political class to picture its state as an actor capable of saying no. Law can be interpreted. Risk can be priced. Imagination is the substrate on which the other two rest. When imagination collapses, law and risk are made to carry weight they were never designed to bear, and the result is the posture we now inhabit: constraints that are technically contestable are treated as constraints that are not.

I use the phrase captive by consent to describe this condition because none of the ordinary vocabulary suffices. We are not, in any technical sense, a colony. We are not, in any honest sense, a negotiating equal. We are a sovereign state that has learned to perform the ritual of sovereignty while declining the substance of it. The 2016 PSA is the document in which that performance is most legible. The politics of resignation is the political formation that keeps it in force.

Sanctity of contracts is not, in the Guyanese case, a principle of law. It is a reputation technology — and the reputation it buys is worth less than what it costs.

Section III

The Mechanics of Leakage

What the architecture of resignation costs us can be stated in terms precise enough to satisfy an auditor. Consider the 75% figure. It is often described, including in my own earlier work, as a “cost-recovery ceiling.” The more accurate description is that it is a monthly maximum deduction with an indefinite carry-forward: costs not recovered in one month roll into the next, and the next, until they are. In practice, this makes the 75% a floor on contractor recovery as long as the consortium’s accumulated costs remain high — which, given the pace of new developments in the block, they do and will. The government’s share of profit oil begins only after the monthly maximum is met. Capital expenditure for the next phase of production deferral is, under this architecture, the state’s problem.

Consider, separately, what ring-fencing would have done. Under a ring-fenced regime, the costs of the Payara development could only be recovered against Payara revenues. Under the 2016 PSA as executed, Payara’s costs are recovered against the combined revenues of Liza Phase 1, Liza Phase 2, Payara itself, Yellowtail, Uaru, and every subsequent tie-back and expansion inside the Stabroek Block. The consolidation is not a rounding error. It is a structural delay, running to years at a time, in the arrival of profit oil at the Natural Resource Fund. Every new well the consortium drills is, in effect, a deferral of our share.

Layered atop this architecture is the auditing problem. A significant audit of costs incurred between 1999 and 2017, amounting to over US$1.7 billion, took years to finalize and was resolved in ways many analysts have considered favorable to the contractor. The Ministry of Natural Resources has acknowledged — in its own annual reports — that the scrutiny of complex financial records from multinational operators exceeds its current staffing and expertise (Ministry of Natural Resources, 2023). This is what capacity asymmetry looks like in operational detail. It is also what “gold-plating” — the inflation of recoverable costs — becomes possible inside of. The IMF has repeatedly urged Guyana to strengthen its audit capability as a matter of first-order fiscal urgency (IMF, 2023). It has not yet happened at scale.

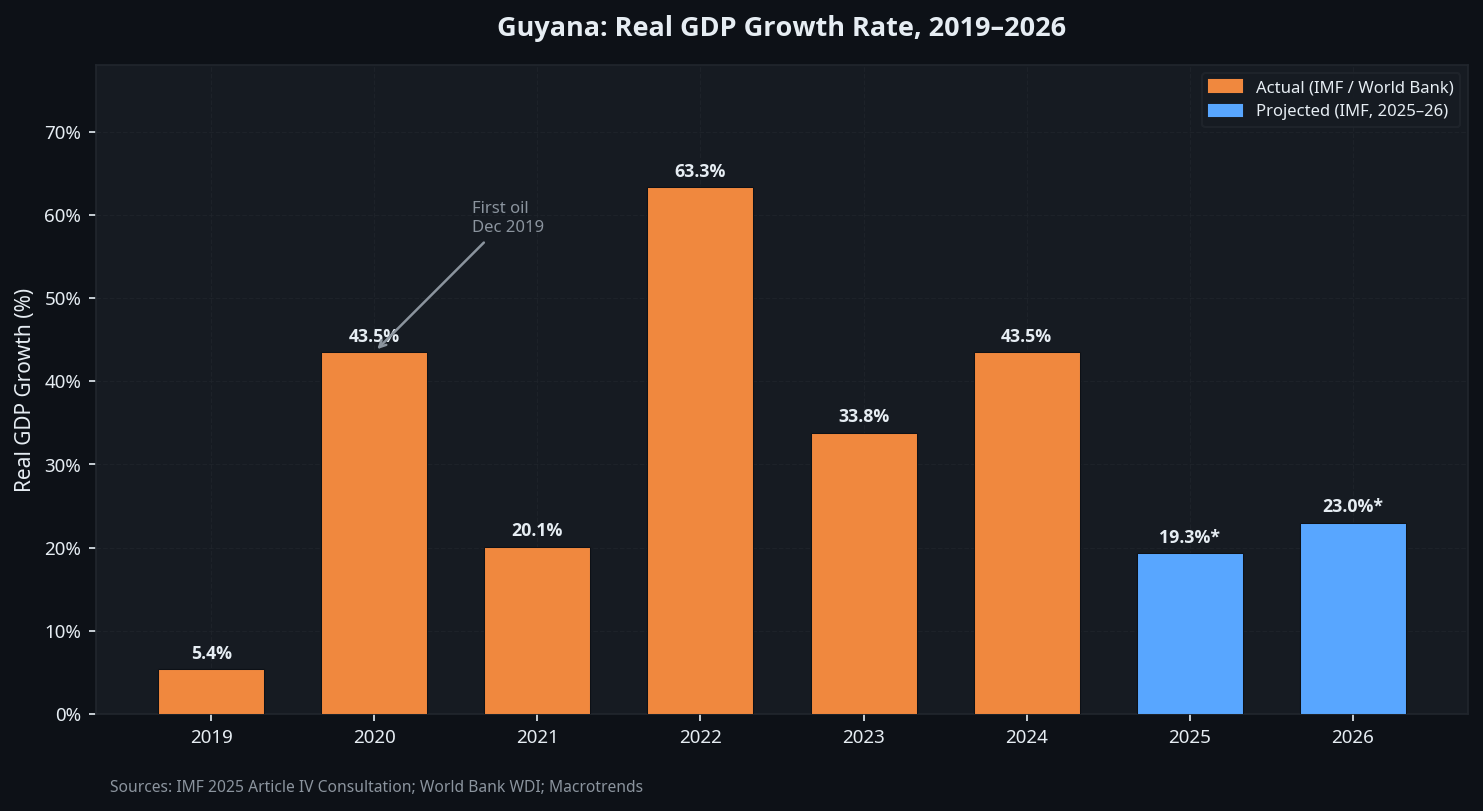

Production has soared from roughly 120,000 barrels per day in late 2021, when only Liza Destiny was operating, to over 900,000 barrels per day by early 2026, with Liza Unity, Prosperity (Payara), and the latest tie-backs in service (Bank of Guyana, 2026). The consortium’s gross revenues have grown accordingly. The state’s share has grown too — but more slowly than production, and very differently than the public conversation assumes. That difference is the price of the architecture.

The 75% is not a ceiling. It is a floor. Every new well the consortium drills is, in effect, a deferral of our share.

Section IV

The Case That Will Not Close

Calls for renegotiation of the 2016 PSA have been a consistent feature of Guyana’s political discourse since the terms became widely known. The argument, in its strongest legal form, rests on the doctrine of changed circumstances: that the terms were agreed under conditions of information asymmetry and geopolitical vulnerability that have since been materially resolved by the proven scale of discovery and the queue of operators who would enter the basin today. In its strongest political form, the argument is simpler. Two administrations, of opposite coalitions, have now governed under these terms. Both have critiqued them. Neither has changed them.

The language in which successive governments have declined to renegotiate is worth attending to, because it is the language in which the architecture of resignation speaks for itself. In 2018, Minister of Natural Resources Raphael Trotman, pressed on the terms his government had signed, said that the government had weighed the benefits against the drawbacks and decided to “content ourselves with” what had been agreed (Stabroek News, 2018). The phrase deserves to be lingered over. To content oneself with is neither to choose nor to be coerced. It is the middle posture — the posture of the administrator who has weighed the argument, declined the harder path, and named the decision a virtue. It is a confession of inadequacy dressed as prudence. And it is, almost word for word, the posture of the PPP/C government that succeeded him.

President Irfaan Ali’s administration, while acknowledging publicly that the 2016 terms are sub-optimal, has declined to pursue renegotiation and has instead directed its policy energy to local content, regulatory oversight, and future agreements. The stated reasons are familiar: contract stability, investor confidence, the risk of protracted arbitration, the signal that renegotiation would send to frontier basins still seeking capital (Guyana Times, 2023). The unstated reason is the one that matters most. Governing inside an inadequate contract is easier than governing the political storm that would follow any serious attempt to alter it. Resignation, as a posture, pays political dividends on the day it is adopted and charges its costs to a future no administration expects to inhabit.

The case for prudence, it must be said, is not frivolous. Contract stability is a genuine public good; rating agencies and bilateral creditors do read signals; an extended ICSID arbitration would delay production and compound costs the treasury cannot easily absorb. A government that inherits a contract it did not write owes its successors some caution about the precedents it sets. The serious version of the prudential argument is that there is a line, and that the line separates what cannot easily be changed from what still can. On the difficult side of the line sit the royalty rate, the profit-oil formula, and the cost-recovery percentage itself — all of which require negotiated amendment with contractual counterparties whose cooperation is not guaranteed. On the other side sit the rigor of the cost audit, the enforcement of local content, the ring-fencing of future tie-backs through regulatory interpretation, the statutory authority of the petroleum regulator, and the transparency mechanisms that determine whether the Guyanese public can even see what its state is owed. The resignation I am describing is not about the difficult side of that line. It is about the other side. It is the political habit of allowing what is merely inconvenient to be treated as if it were legally impossible — and of allowing what can, in fact, be changed this week to remain unchanged across two administrations.

The critics of this posture — Adams chief among them — have dismissed the fear of investor flight as analytically unserious. The 2016 renegotiation itself, Adams notes, set the precedent that these terms are alterable. The proven reserves make Guyana highly attractive. “There is zero chance,” he has written, “that ExxonMobil will walk away under reasonable circumstances; and even if they do… there will be a line of their competition tripping over each other to take their place” (Stabroek News, 2018). The analytical case is strong. The political case remains harder to make — not because the evidence is weaker, but because the architecture of resignation is reinforced every time an elected government declines to test it.

GBJ Data Note

Estimated recoverable resources in the Stabroek Block have grown from approximately 3.2 billion barrels of oil equivalent at the time of the 2016 PSA to over 11 billion BOE by early 2026 (ExxonMobil, 2026). Under the doctrine of changed circumstances, a fourfold expansion in proven reserves is the textbook case for fiscal revision. In the Guyanese case, it has been the textbook case for inaction.

Section V

Local Content as Partial Repair

In the absence of renegotiation, the government has placed significant emphasis on the Local Content Act (2021) as the primary instrument for broadening Guyanese participation in the oil economy. The Act sets participation targets across forty categories of goods and services: ninety percent Guyanese participation in immigration support services and ground transportation, twenty-five percent in drilling and well services by the tenth year, with graduated thresholds across the intermediate categories (Ministry of Natural Resources, 2021). By late 2025, reports from the Local Content Secretariat indicated that approximately fourteen thousand Guyanese were directly employed in the sector and over 1,300 firms had been formally registered under the Act (Guyana Chronicle, 2025; OilNow, 2025).

These figures are real and the policy is serious. The challenges are also real: the capacity of local firms to meet international technical standards, the difficulty of accessing working capital at competitive rates, and the persistent risk of “fronting” — arrangements in which foreign firms use Guyanese partners as a compliance façade. The IMF has noted the importance of a well-designed local content regime while cautioning against protectionist overreach that raises costs without building capability (IMF, 2021). On the ground, the honest assessment is that local content is working, slowly, at the margins where the state can enforce it.

But local content, however well-administered, cannot compensate for the fiscal architecture of the PSA. Royalties and profit oil fund public goods at national scale: the hospitals, the universities, the flood-control infrastructure a coastal country below sea level cannot afford not to build. Local content funds jobs and enterprise one contract at a time. The two operate at different scales and with different multipliers. Local content is a vital artery for economic diversification, but it cannot substitute for the fiscal transfer that a more equitable revenue-sharing regime would have delivered. Or, to put the contrast sharply: local content is repair work. It is not a replacement roof.

Section VI

The Natural Resource Fund and the Mathematics of Inadequacy

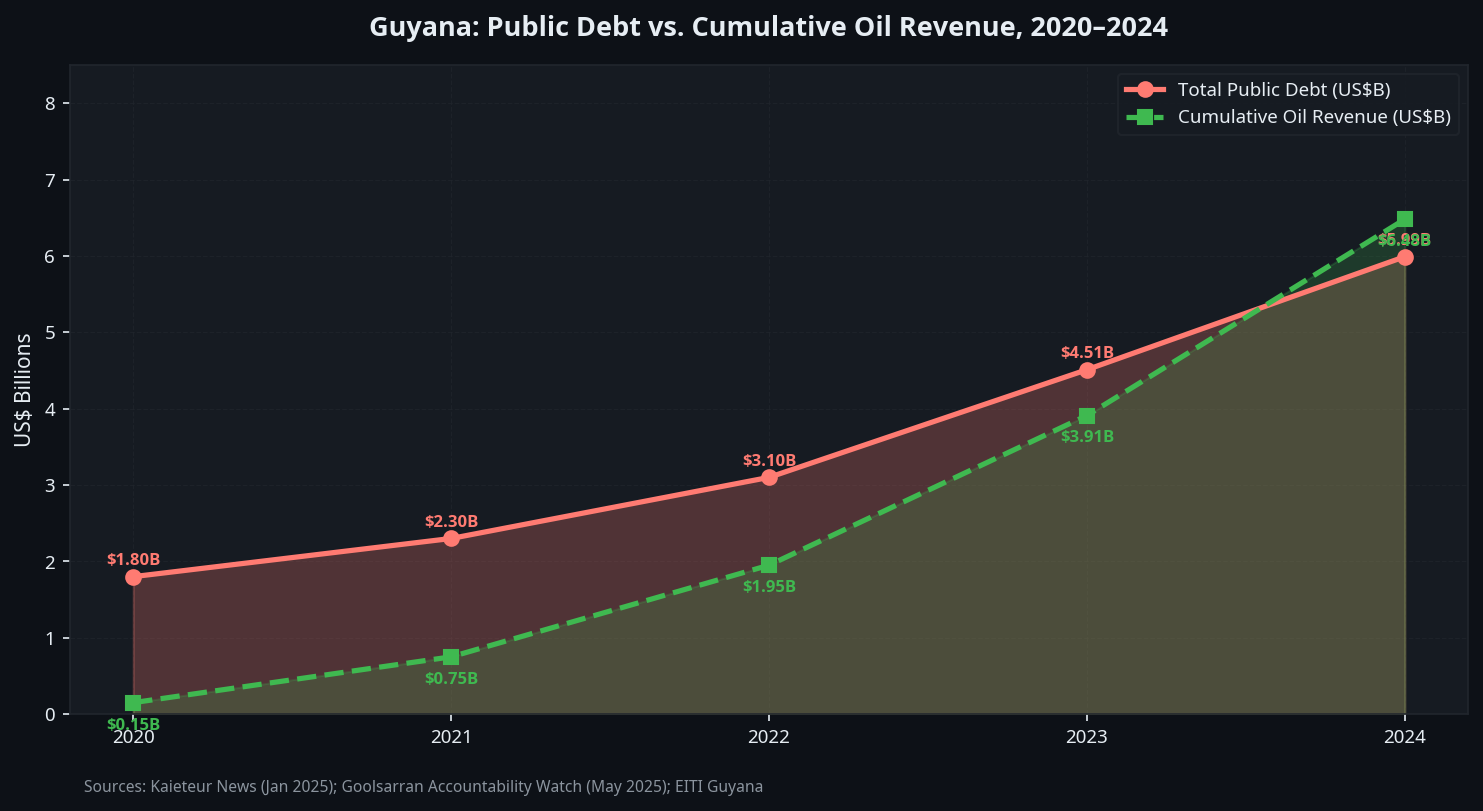

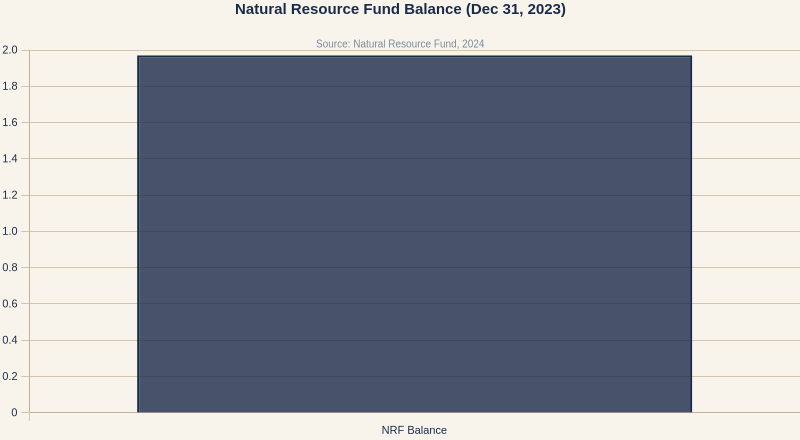

Guyana’s oil revenues are channeled through the Natural Resource Fund, established under the NRF Act (2021) to ensure intergenerational equity and insulate public spending from the volatility of oil markets. The Fund is, institutionally, a serious instrument: its rules are formula-based, its reporting is public, its existence is itself a reply to the cautionary tales of other oil-rich nations. As of December 31, 2025, the NRF balance stood at US$3.25 billion (Bank of Guyana, 2026).

And yet the Fund is an accounting identity, not a protection. Into it flow royalty and profit-oil receipts as the 2016 PSA defines them; out of it flows the fiscal rule as Parliament has enacted it. The gap between the Fund’s rate of accumulation and the Fund’s rate of disbursement is what intergenerational savings, in any technical sense, actually consists of. In 2025, that gap was, by a narrow margin, negative: the Fund received US$2.4 billion in oil revenues — US$330.7 million in royalty and US$2.1 billion in profit oil — and the government withdrew US$2.463 billion over the same period (Natural Resource Fund, 2026). The headline balance grew only because earlier deposits had not yet been drawn down. This is not saving. It is a cadence of deposits and withdrawals that happens to net positive because the deposits, for now, arrive faster than Parliament can spend them.

The macroeconomic consequences of this rhythm are already visible. GDP growth has been, by IMF reckoning, among the highest on record for any economy in the modern era. The inflows of foreign exchange have begun to pressure the non-oil tradables sector in the classic Dutch Disease pattern. The Bank of Guyana has managed the monetary side ably (Bank of Guyana, 2025), but monetary policy cannot substitute for the more fundamental work of diversification, and diversification requires fiscal space the 2016 PSA continues to constrain. Had the agreement been written differently, the Fund would not only hold more; it would be disbursing from a deeper base, with proportionately more flowing to intergenerational savings and proportionately less claimed by the immediate pressure to spend. The mathematics of the Fund, in short, is not independent of the mathematics of the contract. It is downstream of it.

GBJ Data Note

The Natural Resource Fund received US$2.4 billion in oil revenues in 2025 (US$330.7 million in royalty, US$2.1 billion in profit oil) and disbursed US$2.463 billion to the Consolidated Fund over the same period (Natural Resource Fund, 2026). The year-on-year balance increase reflects residual carry-forward from earlier deposits, not current-year saving.

Section VII

The Model PSA and the Road Not Yet Taken

The government has, to its credit, produced a new model PSA for future offshore blocks. The 2022 model raises the royalty to ten percent, lowers the monthly cost-recovery maximum to sixty-five percent, imposes a ten percent corporate income tax, and introduces ring-fencing provisions at the project level (Ministry of Natural Resources, 2022). Each of these represents a material improvement over the 2016 terms. Each of them, taken individually, acknowledges the inadequacy of what was signed in June 2016 without naming it as such. The new model is, in effect, the country’s confession written in the language of future contracts. The state is conceding, in the model, what it declines to concede in the renegotiation.

There is a limit to how much this should comfort us. The Stabroek Block, under the 2016 agreement, will deliver the bulk of Guyana’s current and projected production for the next two decades. The new model will govern blocks smaller in proven resource and slower in development timeline. By the time the new model’s fiscal terms begin to meaningfully alter the state’s revenue profile, the 2016 PSA will have delivered most of what it is going to deliver under the terms it delivers under. The improvement is directional. It is not retroactive.

What the new model does establish is that renegotiation of the legacy agreement is not ruled out by external constraint. The state that wrote the new model is the same state that could, if it chose to, open the 2016 conversation. Nothing in the international legal or commercial environment prevents it. What prevents it is internal: the focal-point equilibrium, the reputation technology, the political calculation that resignation is cheaper than voice. These are the things, to borrow a phrase I have used in other contexts, that institutions are for. They are also the things institutions, in their current Guyanese form, have not yet been built to overcome.

Section VIII

What Sovereignty Requires

The 2016 agreement will continue to govern the Stabroek Block for the better part of the next two decades. This is the architecture we have. But architectures, as Best reminded us, are inhabited. What we do inside them — whether we audit rigorously or audit ceremonially, whether we enforce local content or let it be fronted, whether we build the ministries that can negotiate the next agreement or subcontract that capacity to the consultants who wrote the last one — is still ours to decide.

The project before us is not, in the first instance, to renegotiate a contract. The project before us is to become the kind of state that could have negotiated the contract differently in 2016, and can negotiate the next one differently in 2030. That is a project of institutions, of training, of public reason, of a political culture that does not content itself with terms it knows to be inadequate. It is, in the end, a project of imagination — of believing that we are a polity that gets to choose, rather than a polity that has been chosen for.

Three institutional moves would, without renegotiating a single clause of the 2016 agreement, materially alter its operation. First, the establishment of an independent petroleum commission with statutory authority to audit cost recovery, enforce ring-fencing interpretations, and publish quarterly reconciliations of contractor submissions against recoverable expenditure. Second, the build-out of a standing negotiation capacity inside the state — a permanent technical unit, staffed with Guyanese and diaspora expertise, that serves as the institutional memory for every oil and gas negotiation the country will undertake between now and the exhaustion of the basin. Third, the codification of transparency: the full text of every PSA, every cost-recovery submission, every audit disposition on a public register, auditable by civil society, by the press, and by the Parliament that ratified none of these arrangements. None of these reforms requires ExxonMobil’s consent. None of them risks the arbitration panel we are told to fear. All of them sit squarely within the domestic authority the state already holds. The reason they have not been executed is not legal. It is imaginative.

Walter Rodney, writing about a different commodity and a different century, asked the question this essay has been circling from the first paragraph: will we rest content with the terms of our own diminishment, or will we do the harder, slower, more institutional work of earning the sovereignty we already hold on paper? The question does not resolve in an essay. It resolves, one audit at a time, one budget cycle at a time, one negotiation at a time, across the twenty-year life of the agreement we already signed.

Captive by consent is not a sentence. It is a diagnosis — and a diagnosis that locates the pathology squarely inside the Guyanese state, which means the treatment is available to us without anyone else’s permission. The contract is the past. The audit we commission next quarter, the petroleum commission we either establish or decline to establish, the transparency register we either build or quietly forget, the technical unit we either staff or leave unstaffed — these are not the past. These are the places where the next decade of Guyanese sovereignty is actually decided. And these are the places where resignation, if it is to end, must end.

The pathology is located squarely inside the Guyanese state. Which means the treatment is available to us without anyone else’s permission.

◆ ◆ ◆

Dr. Terrence Richard Blackman is Founder and Publisher of the Guyana Business Journal and Professor and Chair of the Department of Mathematics at Medgar Evers College, City University of New York. He is a former Dr. Martin Luther King Jr. Visiting Professor at MIT and a Visiting Scholar at the Institute for Advanced Study in Princeton. His Transforming Guyana webinar series has convened diaspora scholars, policymakers, and practitioners across North America, the Caribbean, and Europe. He writes on Guyanese political economy, mathematics education, and the political economy of the Caribbean.

References

- Bank of Guyana. (2025). Annual Report and Statement of Accounts. Retrieved from https://bankofguyana.org.gy

- Bank of Guyana. (2026). Quarterly Reports and Press Releases. Retrieved from https://bankofguyana.org.gy

- ExxonMobil. (2026). Guyana Operations Overview. Retrieved from https://corporate.exxonmobil.com/locations/guyana

- Guyana Chronicle. (2025, September 28). Local Content Act driving Guyanese participation in oil and gas sector. Retrieved from https://guyanachronicle.com

- Guyana Times. (2023, October 29). Govt. committed to existing oil contracts – President Ali. Retrieved from https://guyanatimesgy.com

- International Monetary Fund. (2017). Guyana: Staff Report for the 2017 Article IV Consultation. IMF Country Report No. 17/373. Retrieved from https://www.imf.org

- International Monetary Fund. (2021). Guyana: Staff Report for the 2021 Article IV Consultation. IMF Country Report No. 21/249. Retrieved from https://www.imf.org

- International Monetary Fund. (2023). Guyana: Staff Report for the 2023 Article IV Consultation. IMF Country Report No. 23/345. Retrieved from https://www.imf.org

- Kaieteur News. (2023, December 10). ExxonMobil’s Cost Recovery: A Deep Dive into Guyana’s Oil Wealth. Retrieved from https://www.kaieteurnewsonline.com

- Ministry of Natural Resources. (2021). Guyana Local Content Act 2021. Retrieved from https://mnr.gov.gy

- Ministry of Natural Resources. (2022). Guyana’s New Model Production Sharing Agreement. Retrieved from https://mnr.gov.gy

- Ministry of Natural Resources. (2023). Annual Reports and Sector Updates. Retrieved from https://mnr.gov.gy

- Natural Resource Fund. (2021). Natural Resource Fund Act 2021. Retrieved from https://nrfguyana.gov.gy

- Natural Resource Fund. (2026). Monthly and Annual Reports. Retrieved from https://nrfguyana.gov.gy

- OilNow. (2024, January 15). Guyana’s Oil Future: Balancing Contracts and National Interest. Retrieved from https://oilnow.gy

- OilNow. (2025, September 20). Over 1,300 Guyanese firms are now registered under the country’s Local Content Act. Retrieved from https://oilnow.gy

- Rystad Energy. (2022). Fiscal Regime Benchmarking: Guyana vs. Global Peers. (Proprietary report; publicly referenced in industry analyses.)

- Stabroek News. (2018, February 4). Exxon should pay US$1B up front to Guyana, energy expert says. Retrieved from https://www.stabroeknews.com

- Stabroek News. (2022, July 24). Calls for renegotiation of ExxonMobil contract intensify. Retrieved from https://www.stabroeknews.com

- Stabroek News. (2023, September 10). Former Minister defends 2016 oil deal amidst renewed criticism. Retrieved from https://www.stabroeknews.com

Supported By

We are grateful for the partnership and support of individuals and organizations committed to advancing Guyanese and Caribbean development and human capital investment.

Metallica Commodities Corporation

For over two decades, Metallica Commodities Corporation has connected producers and consumers of non-ferrous metals across the Americas, Africa, and Asia. Headquartered in New York with offices in Peru, Canada, Tanzania, and Guyana, MCC brings institutional expertise and global reach to resource-rich markets, with a deep understanding that sound governance determines whether natural wealth generates broad-based prosperity.

The GBJ Sunday Essay is supported by MCC and is not written on its behalf. The views expressed are those of the author.

METALLICACC.COM ↗Pebble Stream™

Pebble Stream™ is a US-based cloud-computing company that transforms complex Excel models into secure, enterprise-scale cloud applications through patented “pebblization” technology. Founded by Bediako George and backed by over 25 years of financial and accounting expertise, the company processes one billion tax calculations monthly and counts a Big Four accounting firm among its clients. For Guyanese and Caribbean businesses, Pebble Stream offers the scalability a rapidly growing economy demands.

This GBJ article is sponsored by Pebble Stream™ and is not written on its behalf. The views expressed are those of the author.

PEBBLESTREAM.COM ↗Caribbean International Shipping Services

Ship with Confidence: Your Trusted Logistics Partner

For over 30 years, Caribbean International Shipping Services has been the trusted choice for businesses and individuals shipping from the Southeast USA to the Caribbean and Latin America. Specialising in household relocations, commercial goods, and online order consolidation, their experienced team delivers weekly ocean and air freight services to over 20 destinations — reliably and stress-free.

📞 770-322-3111

CARIBSHIPATL.COM ↗MCCGUSA

Management Consulting, Project Management, Real Estate

Founded in 1990, MCCGUSA (formerly Management Consulting and Controls Group) is a premier consulting and project management firm serving clients across the United States and internationally. A Certified MBE, DBE & Hub Zone Business, MCCGUSA provides management consulting, project management, financial advisory, and real estate services — with national affiliates and international representation in the Caribbean and Latin America.

📞 212-269-6126

MCCGUSA.COM ↗Individual Supporters

Courtney Allen | All Te Networks | Corine Locke | Tony Harris | Roderick Alsopp | Dr. Michelle Luard | Clarence Bone

🇬🇾 Please support the Guyana Business Journal & Magazine today