Understanding Guyana’s Central Bank Reserve Balances: An Insider’s Guide

by

Joel Bhagwandin

Summary

The Bank of Guyana’s (BOG) capital and reserve account balances are not the country’s reserve. The reserve balances reflected on the Capital, Liabilities, and Reserves side on the Bank’s balance sheet are part of the institutional capital structure of the Bank. Conversely, the country’s reserves held by the Bank are reflected on the asset side of the Bank’s balance sheet―which constitutes market securities, special drawing rights (SDR) holdings, foreign balances, and gold reserves. Furthermore, it is essential to note that reserve management is one of the core functions of the central bank to meet its objectives which include price stability, meeting inflation targets, and exchange rate stability. Within this framework, it is also important to highlight that central banks exist to achieve the policy objectives prescribed in their respective laws. These cover monetary policy and systemic stability targets in pursuit of broader macroeconomic objectives. Therefore, rather than resource utilization or profitability efficiency, policy effectiveness provides the basis for central bank accountability.

Background

A recent news report posited that the Bank of Guyana’s profit could not meet the country’s reserve. The report cited a negative balance on the bank’s balance sheet as of February 2023, which was $12.1 billion. However, the explanation in the article attributed to this negative balance was without any analysis and, more so―void of an understanding of the purpose and function of the central bank’s reserve.

This article, therefore, seeks to address this issue by attempting to provide a sufficient explanation grounded in academic literature in terms of the purpose and function of the reserves and the implications of a negative balance.

Discussion and Analysis

The Bank of Guyana’s (BOG) capital and reserve account balances are not the country’s reserve. However, the reserve balances reflected on the Capital, Liabilities, and Reserves side on the Bank’s balance sheet are part of the institutional capital structure of the Bank.

Conversely, the country’s reserves held by the Bank are reflected on the asset side of the Bank’s balance sheet―which constitutes market securities, special drawing rights (SDR) holdings, foreign balances, and gold reserves. As of February 2023, the BOG’s total foreign assets stood at G$168.4 billion or US$807 million. This also corresponds to the net international reserve as per the “International Reserves and Foreign Assets” table 3.2 in the bank’s statistical report for February 2023.

Bank of Guyana Capital and Reserves

The capital and reserve balances of the central bank constitute several reserve accounts: the paid-up capital, general reserve fund, revaluation reserves, revaluation for foreign reserves, contingency reserves, and other reserves. Therefore, the referenced news report’s negative balance is attributed to the adjustments made in the revaluation reserve account. However, the revaluation reserves are not to be treated in isolation from the other reserve accounts of the Bank. Instead, it is treated as part of the bank’s total capital and reserve base―that is to say, the computation of the total reserve balance includes the balance in all of the reserve accounts, as previously mentioned. Consequently, any negative balance in the revaluation reserve will be reduced with positive balances in the other reserves, further offset by the net profit generated by the Bank.

While the gazetted statement of assets and liabilities for February 2023 reflected a negative balance of $9.1 billion, the statistical report published by the Bank for that month showed that the “other reserves” balance stood at $4.3 billion in the negative.

The revaluation reserve of the Bank reflects adjustments made for gains or losses derived from changes in the market value for the assets and liabilities of the Bank, specifically foreign assets and liabilities. To maintain the adequate capacity to fulfill its functions, the Bank has adopted a prudent approach to provisioning prescribed in the Bank of Guyana Act. Section 7 of the Act allows for deducting provisions before declaring profit and payment into the Consolidated Fund. The provision is to meet adverse market movements for investments held and other risks (market, credit, and interest rate) which may occur. So, for example, the bank holds gold as part of its total reserves. Gold prices tend to fluctuate based on market conditions which means that the price of gold at the beginning of the financial year may experience an upward or downward movement at the end. Therefore, whatever the market value of this asset at the end of the financial year, the adjustment is made accordingly, which is reflected either as a gain or loss in the revaluation reserves account. The same principle and practice apply to the Bank’s other financial instruments as part of its total foreign asset portfolio.

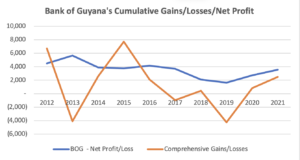

The gains and losses arising from a change in the fair value of available-for-sale assets are recognized directly in equity. However, when the financial assets are sold, collected, or otherwise disposed of, the cumulative gains or losses on the disposal are recognized in the income statement. To demonstrate this point, 2012-2021, 2013, 2017, and 2019 recorded losses of $4 billion, $953 million, and $4.2 billion, respectively. However, the cumulative gains and net profit for the same period amounted to $13.5 billion and $35.6 billion, respectively―as illustrated in the chart below.

Source: Bank of Guyana/Author

Concluding Remarks

Furthermore, it is essential to note that reserve management is one of the core functions of the central bank to meet its objectives which include price stability, meeting inflation targets, and exchange rate stability. Within this framework, it is essential to highlight that central banks exist to achieve the policy objectives prescribed in their respective laws. These cover monetary policy and systemic stability targets in pursuit of broader macroeconomic objectives. Policy effectiveness, rather than efficiency in resource utilization or profitability, provides the basis for central bank accountability.

About the Author

Joel Bhagwandin is a financial, economic, and public policy analyst. He is also an entrepreneur with over fifteen years of experience in the financial sector; corporate finance; financial management; consulting, and academia. He has provided insights and analyses on various public policy, economic, and finance issues in Guyana for the past 6+ years. He has authored more than 300 articles covering a variety of thematic areas. Joel has also written extensively on the oil and gas sector. Joel holds an MSc in business management with a specialism in banking and finance from Edinburgh Napier University. He is currently pursuing his second and third masters: 1) MBA (Finance) (Top-up) through Edinburgh Napier University, and 2) MSc. in Finance (Economic Policy) through the University of London.

References:

- https://www.kaieteurnewsonline.com/2023/03/21/bank-of-guyana-profits-unable-to-maintain-countrys-cash-reserves/.

- https://www.bis.org/publ/othp04_2.pdf.

- https://www.bis.org/publ/bppdf/bispap104.pdf.

- https://mola.gov.gy/sites/default/files/Cap.%208502%20Bank%20of%20Guyana.pdf.